The Art of Deceiving Citizens Through Maintained Ignorance

When citizens' funds are managed without shame, a dangerous social pattern emerges.

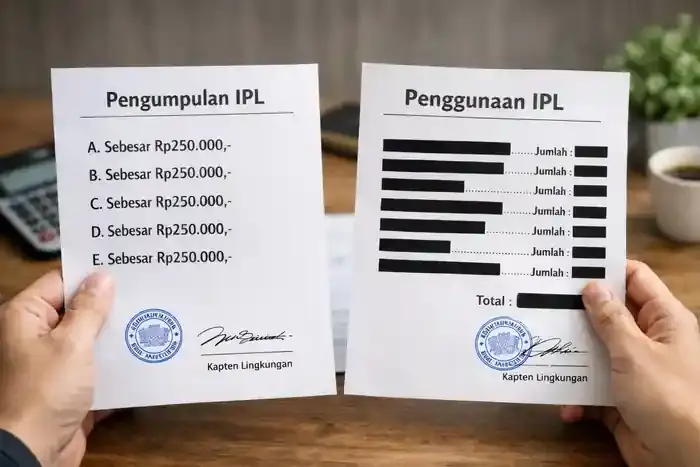

Income funds are announced in detail and repeatedly, while expenditures are hidden or censored. This is not administrative negligence, but a manipulation of public perception—a new form of social fraud legalized by collective ignorance.

Name of the Social Disease: Pseudo-Financial Transparency

In governance literature, this practice is known as Selective Disclosure Fraud: revealing information that benefits fundraising while hiding information that may raise questions.

Its characteristics are simple:

- Income is announced in detail and the amounts are clear to build social proof.

- Expenditures are not explained or the terms are obscured.

- Criticism is considered disruptive to togetherness.

This is not transparency; this is a fake showcase.

Why Is Income Flaunted?

Announcing funds is not just a report, but a psychological tool to entice others to donate. Large figures create an illusion of legitimacy, and the public is driven not to "appear stingy." When expenditures are questioned, the narrative changes to: “Already as needed” or “Just trust each other.” Trust is exploited, not maintained.

Moreover, fundraising clickbait is common: the donation from one donor A is exaggerated and announced prominently. The goal is not transparency, but to lure other donors to contribute because they are influenced by the “large number.” Essentially, this is just a psychological bait, not an indication of actual fund usage.

Read other articles as well:

Accounting Aspect: Donation Poster, Not Financial Report

A proper financial report requires structure, completeness, and honesty. Information must be relevant, complete, verifiable, and not misleading. In current widespread practice: income is highlighted, expenditures are obscured, audits are difficult, and evidence is unavailable.

Without detailed expenditures, transaction evidence, and clear allocations, the report is merely a one-sided list of income disguised as legitimate.

Why This Is Not a Financial Report?

- Only the income side is flaunted.

- Expenditures are obscured; evaluation and verification are impossible.

- Accountability is lost.

The result: this is a donation poster masquerading as accounting.

What Audit Category Does This Fall Under?

This practice falls under Material Omission, the omission of critical information that affects public decision-making. The consequences are:

- The public donates based on incomplete information.

- Financial decisions are made under information asymmetry.

- Trust is built on missing data.

This is information manipulation, not public negligence.

Common Arguments and Why They Fail

“This is not a company.” Wrong. Accountability comes from the source of funds. Once money comes from many people: public rights are inherent, responsibility is mandatory, and “just trust” is not an accounting principle. Trust without data = invitation to abuse.

“Donors are willing and sincere, right?” Wrong. This is not about donors’ intentions, but from the recipient’s side and accounting practice.

Accounting Conclusion

- Reports without expenditures = incomplete reports.

- Reports without evidence = empty claims.

- One-sided reports = manipulation tools.

Manipulation remains manipulation, even when wrapped in numbers and slogans of togetherness. Accounting only demands honest numbers that can be tested.

Legal Aspect

Public funds carry legal consequences:

- Fraud Element: if fund usage is not in accordance with the stated purpose or not explained.

- Breach of Trust: managers fail to report in detail or block access to information.

- Collective Accountability: fund managers are legally responsible.

Why Does This Practice Persist?

The public is conditioned to stay silent: asking questions is considered rude, requesting reports is seen as suspicious, transparency is considered optional. Yet public money without detailed reporting = invitation to conflict.

Real Impacts If Left Unchecked

- Loss of long-term trust.

- Internal conflicts and accusations.

- Collective reputation damage.

- Potential legal issues.

- Normalization of social fraud as “common practice.”

Ironically, the slogan “From us, for us” hides the reality: from many people, for a few who refuse to explain.

Minimal Transparency Standards

A truthful report must include: date of expenditure, recipient name, purpose of use, amount per item, and transaction evidence (at least a summary). Without this, claims of trustworthiness are empty.

Conclusion: Honesty Never Fears Detail

True transparency does not fear numbers, questions, or details. Those who fear usually hide ulterior motives. The public has the right to know.

FAQ

- Are administrators required to open expense reports?

Yes, the public's right to know always applies. - Is just an expense report enough?

No, because it does not explain where the money goes. - What if a report is requested but not provided?

This is a serious red flag and may constitute a legal violation. - Can non-contributors request reports?

Absolutely, legally, because fundraising falls under the community, whether a contributor or not. - Are social funds free from audit?

Not at all; social funds are more sensitive because they rely on trust and their purpose must be clear. - What is the role of citizens/donors?

Ask questions, request reports, and do not fear being labeled critical. Silence fuels social fraud.

Read other articles as well:

- The Invisible Power Mystery in Community Management

- Project Transparency in the Community

- Beware of Fund Hunters on Major Days

- The Role of Buzzers in the Community

- The Magic Trick of Expense Reports in Communities

{kind=link}